The Distribution Partner Equation: How Foreign Innovators Should Structure Their India Entry Economics

- Mamta Devi

- 15 hours ago

- 5 min read

Written By: Jagriti Shahi

When foreign innovators enter India, they often spend months debating the wrong question.

They compare distributor candidates. They negotiate margin points. They evaluate entity structures, GST registration, tender eligibility, and dealer reach.

But the real question is simpler:

How much of the India-entry burden should the local partner actually carry?

That is the equation that determines whether a foreign company survives long enough to scale in India.

And it matters across sectors — agritech, watertech, industrial cleantech, deeptech, climate infrastructure, precision manufacturing, energy systems, and industrial automation all face the same structural reality:

India is not merely a sales market. It is an execution market.

The partner who carries execution risk usually controls the commercial outcome.

The Structural Mistake Most Foreign Companies Make

Most foreign innovators entering India make one of two extreme decisions:

Model 1 — “We fund everything”

The foreign company pays for:

market development

regulatory approvals

demo deployments

distributor onboarding

sales hiring

technical support

government relationship building

tender participation

pilot financing

marketing and events

working capital support

The local distributor simply sells.

This looks attractive at first because the innovator retains control.

But in practice, the distributor becomes a low-risk reseller with limited incentive to prioritize the product.

India is a relationship-heavy operating environment. If the local partner has little capital, credibility, or operational exposure tied to the success of the business, attention shifts quickly toward easier revenue streams.

The result:

slow market penetration

poor distributor commitment

weak after-sales execution

inconsistent government engagement

high burn for the foreign company

Model 2 — “The partner does everything”

At the opposite extreme, some innovators attempt a pure licensing or master-distribution structure.

The local partner:

funds inventory

builds the channel

hires the team

handles support

finances pilots

carries receivables

owns state relationships

The foreign company supplies technology and waits for royalties.

This also fails surprisingly often.

Why?

Because the Indian partner eventually behaves rationally:

they demand exclusivity,

negotiate aggressive pricing,

deprioritize brand-building,

or replace the foreign technology entirely once market understanding improves.

At 100% partner-funded execution, the innovator risks becoming a component supplier instead of a strategic company.

The Real Answer Is Usually the Middle

The strongest India-entry structures sit between those two extremes.

The optimal structure is usually a shared-risk distribution model, where both sides carry

meaningful operational exposure.

The foreign innovator contributes:

technology,

brand credibility,

training,

technical architecture,

partial market-development funding,

strategic account support.

The Indian partner contributes:

distribution infrastructure,

regional relationships,

field execution,

local staffing,

tender access,

dealer management,

receivables management,

regulatory navigation,

and increasingly, co-investment.

That middle zone creates aligned incentives.

When both parties carry cost exposure:

both sides stay commercially engaged,

channel discipline improves,

market feedback loops accelerate,

and long-term economics become more sustainable.

Why India Magnifies Distribution Economics

India’s operating environment amplifies channel economics more than many foreign companies initially expect.

Margins are not simply compensation for sales.

Margins compensate for:

fragmented geography,

receivables risk,

multi-state operations,

dealer financing,

government payment delays,

field support,

seasonal demand swings,

logistics complexity,

and relationship maintenance.

This is why distributor structures in India often appear “expensive” to foreign firms.

But they are compensating for real operating friction.

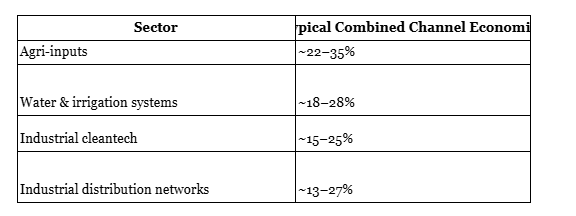

Research across Indian sectors shows broad margin expectations such as:

These structures vary by geography, credit terms, technical complexity, and government exposure, but the pattern is consistent:

India rewards execution-heavy channel partners.

The Government Procurement Reality

Foreign innovators also underestimate how procurement timelines affect distribution economics.

In sectors tied to:

irrigation,

infrastructure,

sustainability,

industrial systems,

municipal deployment,

energy,

or agriculture,

government-linked sales cycles matter enormously.

And those cycles are slow.

India’s procurement ecosystem — including public procurement systems like the Government e-Marketplace (GeM) — often requires:

extensive documentation,

vendor onboarding,

local references,

compliance approvals,

state-level coordination,

and extended payment cycles.

This creates working-capital pressure.

A distributor funding inventory for 120–180 days without shared support eventually loses interest unless margins compensate for that risk.

This is one reason many India entries fail after promising pilot phases: the economics collapse before scale arrives.

The Netafim Lesson

A useful example is Netafim in India.

Rather than operating as a pure exporter into India, the company built deep local integration:

manufacturing capacity,

dealer networks,

agronomic support,

financing structures,

and participation in state irrigation programs.

Over time, the company developed a large local distribution ecosystem spanning thousands of dealers and government-linked deployments.

The key lesson is not irrigation-specific.

The lesson is structural:

Netafim succeeded because it localized execution economics — not just product distribution.

The John Deere India Pattern

John Deere followed a similar logic in India.

The company did not simply export tractors.

It invested in:

dealer ecosystems,

localized manufacturing,

financing access,

after-sales support,

and long-term channel infrastructure.

India rewarded operational commitment.

That pattern repeats across sectors: foreign firms that localize execution economics tend to survive longer than firms attempting lightweight market access.

BASF and the Importance of Channel Depth

BASF also demonstrates another important India-entry principle:

deep distribution matters more than initial visibility.

In India, especially across industrial and agricultural markets, the company with:

stronger field relationships,

better technical support,

and more durable dealer economics

often outperforms technically superior competitors.

The Indian market frequently rewards operational consistency over product novelty.

The Hidden Variable: Working Capital

Many foreign founders focus only on gross margin.

India requires focus on:

receivables,

inventory financing,

dealer credit,

and deployment cash cycles.

In multiple Indian sectors, effective receivable cycles can extend well beyond western norms. Some agri-linked channels can stretch to 90–150 days depending on seasonality and procurement exposure.

This is why partner cost-sharing becomes strategically important.

If the foreign innovator funds everything:

burn becomes unsustainable.

If the distributor funds everything:

commitment weakens unless margins become excessive.

The optimal structure usually involves:

co-funded pilots,

shared staffing,

milestone-linked incentives,

regional exclusivity tied to performance,

and phased transfer of commercial responsibility.

The India Entry Curve Most Companies Never Model

There is usually a nonlinear relationship between:

foreign-company control,

local-partner investment,

and long-term returns.

At 0% partner participation:

the innovator burns cash rapidly.

At 100% partner participation:

the innovator loses strategic leverage.

The strongest outcomes tend to emerge in the middle: where the partner carries enough operational exposure to remain committed, while the innovator retains enough strategic involvement to protect brand, technology, and long-term market positioning.

That middle zone is the real India-entry sweet spot.

And it is rarely achieved accidentally.

What Foreign Innovators Should Actually Negotiate

Instead of negotiating only:

distributor margin,

territory rights,

or annual sales targets,

foreign innovators should negotiate:

1. Cost-sharing architecture

Who funds:

demos,

pilots,

technical hires,

exhibitions,

and working capital?

2. Receivable ownership

Who absorbs delayed payment cycles?

3. Market-development obligations

Who builds awareness versus simply fulfilling orders?

4. Government engagement responsibility

Who handles tenders, registrations, and compliance relationships?

5. Transition triggers

At what scale does the model evolve from distributor-led to direct-market operations?

India Is Not a “Distributor Market”

This is the final misconception many foreign companies carry into India.

India is not merely a distributor market.

It is a shared-execution market.

The companies that win are rarely the companies with:

the best technology,

the lowest manufacturing cost,

or the strongest global reputation.

The winners are usually the companies that structure incentives correctly between:

foreign innovation,

local execution,

and long-term operational commitment.

That is the real distribution partner equation.

And in India, the equation matters more than the product.

Global Launch Base helps international startups expand in India. Our services include market research, validation through surveys, developing a network, building partnerships, fundraising and strategy revenue growth. Get in touch to learn more about us.

"AI-Generated Content Disclaimer: This content was generated in part with the assistance of artificial intelligence tools. While efforts have been made to review, edit, and ensure accuracy, completeness, and reliability, the content may contain errors or omissions. It should not be considered professional advice, and users should independently verify any information before making decisions based on it. The publisher/author assumes no responsibility or liability for any consequences resulting from reliance on this content.".

Comments